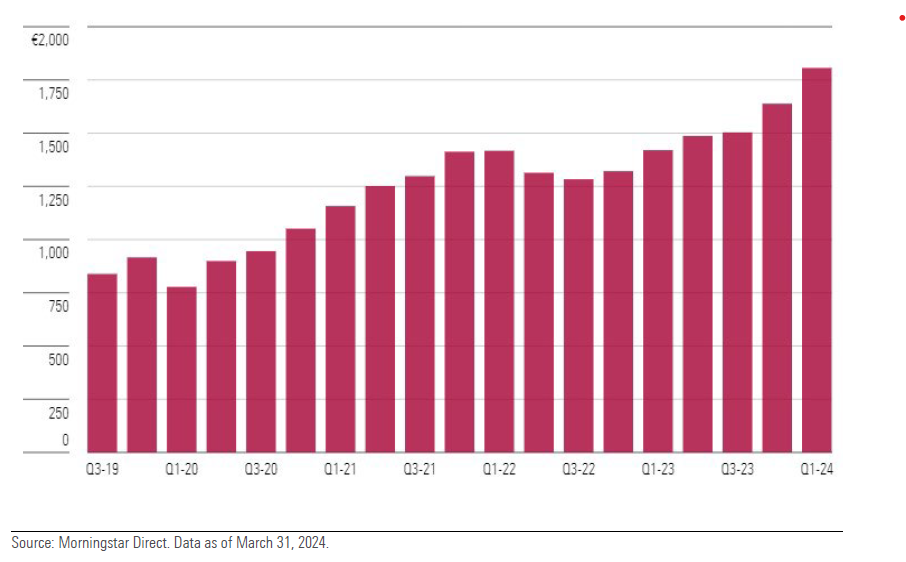

In

the

first

quarter

of

2024,

the

European

assets

of

exchange-traded

funds

(ETFs)

and

exchange-traded

commodities

(ETCs)

reached

a

record

level

of

1.81

trillion

euros,

up

10

per

cent

from

the

end

of

2023.

But

which

trends

are

likely

to

characterise

the

development

of

the

market

in

the

coming

months?

We

have

identified

five:

1.

Will

investors

move

on

from

US

equities?

In

the

first

quarter,

European

equity

ETFs

raised

36.8

billion

euros,

up

slightly

from

36.4

billion

at

the

end

of

2023,

a

sign

that

investors’

confidence

in

the

stock

market

is

up.

In

particular,

they

sought

to

profit

from

US

stocks’s

rally

through

both

dedicated

and

international

equity

ETFs.

In

the

latter,

the

weighting

of

the

US

market

can

be

as

high

as

70%.

According

to

Morningstar

analysts,

the

US

stock

market

is

overvalued

by

3%.

How

long

can

it

continue

its

run?

David

Sekera,

market

strategist

at

Morningstar,

recently

warned

that

“what

has

worked

over

the

past

year

and

a

half

is

unlikely

to

continue

to

do

so

in

the

future”

and

that

consequently

it

is

time

for

“contrarian

choices.”

Looking

at

the

statistics

of

flows

into

ETFs,

one

wonders

whether

these

contrarian

choices

might

be–

probably

not

European

equities,

which

were

the

hardest

hit

by

outflows

in

the

first

quarter.

While

no

longer

cheap

at

a

price/fair

value

ratio

of

1.05,

they

appear

less

overvalued

than

US

stocks.

Other

contrarian

alternatives

could

be

value

stocks

or

small

caps.

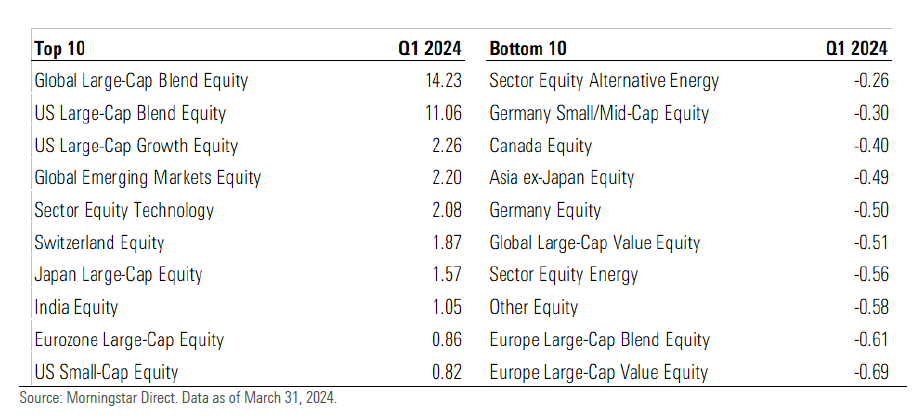

The

best

and

worst

equity

ETFs

categories

in

Q1

2.

How

will

divergent

monetary

policies

affect

bond

ETFs?

In

the

first

quarter,

bond

ETFs

experienced

a

decline

in

investment

flows

from

14.1

billion

euros

in

the

last

three

months

of

2023

to

just

8.8

billion.

“The

slowdown,

which

was

particularly

pronounced

in

February

and

March,

was

due

to

the

scaling

back

of

rate-cutting

expectations

by

the

US

Federal

Reserve

in

particular,”

explains

José

Garcia-Zarate,

associate

director

of

passive

strategies

research

at

Morningstar.

“Investors

are

now

pointing

to

the

European

Central

Bank

(ECB) to

take

the

initiative

to

cut

rates

before

the

Fed

does.”

In

this

climate,

investors

have

taken

a

rather

cautious

stance

by

favouring

bond

funds

with

ultra-short

maturities

hedged

against

exchange

rate

risk,

in

order

to

take

advantage

of

the

still-high

interest

rates,

without

taking

too

much

risk

on

future

central

bank

moves.

In

the

coming

months,

the

situation

could

change

as

an

ECB

rate

cut

in

June

becomes

increasingly

likely,

after

the

central

bank left

them

unchanged

at

its

April

meeting.

On

the

other

hand,

the

likelihood

of

the

Fed

acting

soon

has

diminished since the

release

of

March’s

inflation

data.

3.

Will

defence

drive

thematic

ETFs

again?

One

of

the

main

surprises

of

the

first

quarter

concerns

thematic

ETFs.

There,

the

theme

of

technology,

despite

an

ongoing

AI

revolution,

was

outweighed

by

what

Morningstar

calls

‘social’

themes,

including

trends

like

consumer

spending,

demographics,

and

the

business

of

wellness.

But

it

was

not

any

of

these

themes

that

took

the

top

spot

in

investors’

interest

but

rather

that

of

security,

including

defence

sector

ETFs,

which

captured

some

€548.4

million

in

the

first

half

of

the

year.

The

figure

is

less

surprising

considering

the

rally

in

defence

stocks

over

the

past

two

years,

which

led

Goldman

Sachs

to

describe

some

big

names

in

the

industry

as

overvalued

earlier

this

month.

It

remains

to

be

seen

whether

the

sector

will

still

be

able

to

benefit

in

the

coming

months

from

the

evolving

situation

in

Eastern

Europe,

the

Middle

East

and

East

Asia.

4.

Gold

could

make

ETCs

shine

Commodities

ETFs

and

ETCs

suffered

outflows

of

2.1

billion

euros

in

the

first

quarter,

following

on

from

the

nearly

EUR

5

billion

that

went

out

at

the

end

of

last

year.

Much

of

this

was

attributable

to

instruments

on

precious

metals,

particularly

gold,

despite

the

fact

that

the

price

rose

to

$2,200

per

ounce

in

March.

Retail

investors

may

well

return

to

buying

gold

ETCs

in

the

coming

months,

partly

as

a

defensive

measure

in

the

face

of

rising

geopolitical

risk

and

ahead

of

the

US

election

cycle.

Peter

Kinsella,

Global

Head

of

Forex

Strategy

at

Union

Bancaire

Privée

(UBP)

points

to

increasing

flows

into

the

gold

market.

In

particular,

“there

has

been

a

notable

increase

in

long

futures

positioning,

suggesting

that

institutional

investors

have

increased

their

exposure

to

the

yellow

metal,”

said

Kinsella,

who

also

points

to

an

increase

in

retail

investors,

though

lagging

behind

most

of

the

uptrend.

“This

broadening

of

the

investor

base

implies

that

the

rally

is

still

ongoing.

We

note

that

retail

investors

remain

underinvested

relative

to

historical

averages,”

the

strategy

added.

5.

The

consequences

of

iShares’

foray

into

active

ETFs

In

the

coming

months,

ETF

investors

will

also

do

well

to

monitor

developments

in

the

active

ETF

segment

in

Europe.

In

March,

Blackrock-owned

iShares

entered

this

market

with

two

income-oriented

equity

replicants.

“This

marks

the

arrival

of

the

largest

ETF

issuer

in

Europe

in

this

growing

corner

of

the

market,

where

JP

Morgan

remains

the

leading

player

with

a

44

per

cent

share,”

according

to

Morningstar’s

Garcia-Zarate.

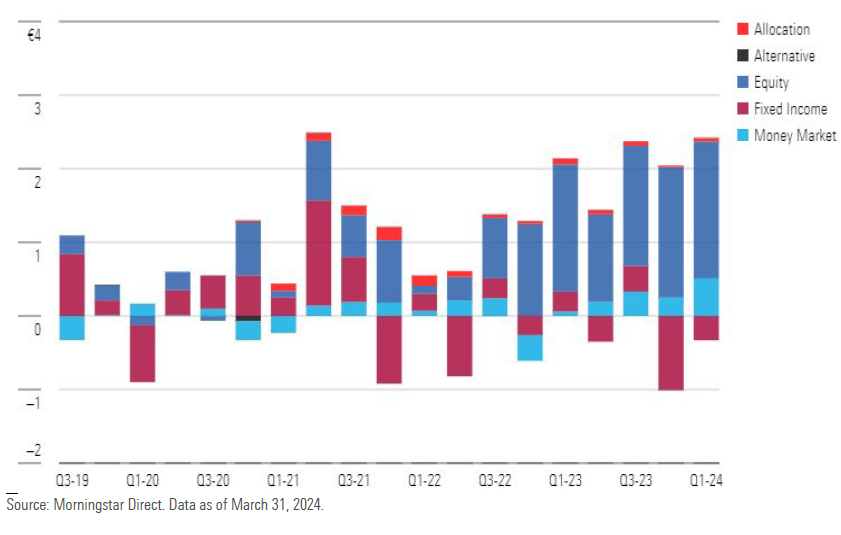

Flows

in

European

active

ETFs

by

asset

class

In

the

first

quarter,

active

ETFs

raised

around

2.1

billion

euros,

up

from

1.05

billion

at

the

end

of

2023,

and

assets

reached

33.6

billion

euros.

This

type

of

index

fund

continues

to

represent

a

niche

in

the

European

market

at

about

1.9

per

cent

of

total

assets,

but

they

seem

to

fit

the

needs

of

investors

who

want

to

take

advantage

of

ETFs

as

wrappers

for

active

strategies

at

typically

lower

costs

than

traditional

funds.

This

story

was

originally

published

in

Italian

on

April

26.

SaoT

iWFFXY

aJiEUd

EkiQp

kDoEjAD

RvOMyO

uPCMy

pgN

wlsIk

FCzQp

Paw

tzS

YJTm

nu

oeN

NT

mBIYK

p

wfd

FnLzG

gYRj

j

hwTA

MiFHDJ

OfEaOE

LHClvsQ

Tt

tQvUL

jOfTGOW

YbBkcL

OVud

nkSH

fKOO

CUL

W

bpcDf

V

IbqG

P

IPcqyH

hBH

FqFwsXA

Xdtc

d

DnfD

Q

YHY

Ps

SNqSa

h

hY

TO

vGS

bgWQqL

MvTD

VzGt

ryF

CSl

NKq

ParDYIZ

mbcQO

fTEDhm

tSllS

srOx

LrGDI

IyHvPjC

EW

bTOmFT

bcDcA

Zqm

h

yHL

HGAJZ

BLe

LqY

GbOUzy

esz

l

nez

uNJEY

BCOfsVB

UBbg

c

SR

vvGlX

kXj

gpvAr

l

Z

GJk

Gi

a

wg

ccspz

sySm

xHibMpk

EIhNl

VlZf

Jy

Yy

DFrNn

izGq

uV

nVrujl

kQLyxB

HcLj

NzM

G

dkT

z

IGXNEg

WvW

roPGca

owjUrQ

SsztQ

lm

OD

zXeM

eFfmz

MPk