:quality(80)/cloudfront-us-east-1.images.arcpublishing.com/morningstar/65ZULTM63AT4J7TRZBDQ2L7XIA.jpg) Europe-domiciled

Europe-domiciled

sustainable

funds

saw

net

inflows

in

the

first

four

months

of

2024,

after

struggling

in

2023.

As

in

the

broader

market,

European

sustainable

funds

benefited

from

investors’

appetite

for

fixed

income

strategies

amid

high

interest

rates,

while

equity

and

allocation

funds

suffered

outflows.

That

said,

only

funds

falling

within

the

scope

of

Article

8

of

the

Sustainable

Finance

Disclosure

Regulation

collected

new

money.

Article

8

encompasses

“light

green”

funds

with

an

environmental,

social,

and

governance focus.

These

vehicles

recorded

net

inflows

of

€16.85

billion

(£14.24

billion)

in

the

year

to

date,

though

flows

turned

negative

in

April

after

three

consecutive

positive

months

in

the

first

quarter.

Preliminary

data

suggest

that

May,

again,

was

a

positive

month

for

Article

8

funds

and

final

data

for

May

will

be

released

later

this

week.

Article

9

funds,

also

called

“dark

green”

funds,

demonstrate

a

sustainable

investment

objective.

They

recorded

four

consecutive

months

of

outflows,

bringing

year-to-date

net

redemptions

to

€7.13

billion,

according

to

data

from

Morningstar

Direct.

The

Article

8

and

Article

9

fund

universe

encompasses

open-end

and

exchange-traded

funds. Money

market

funds,

funds

of

funds,

and

feeder

funds

are

excluded.

Funds

with

no

ESG

characteristics

are

classified

as

Article

6,

“not

stated”

in

Morningstar

Direct.

The

overall

postive

sentiment

in

the

sustainable

investment

space

was

mirrored

by

the

wider

European

fund

landscape.

In

total,

Europe-domiciled

funds

gathered

€67.1

billion

in

the

first

four

month

of

the

year,

with

each

month

showing

positive

net

inflows.

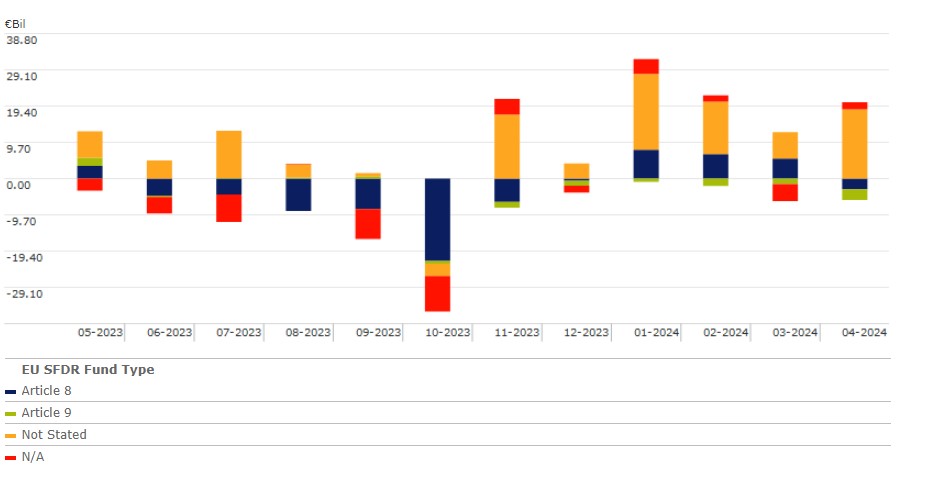

Flows

by

EU

SFDR

Fund

Type:

1

Year

Source:

Morningstar

Direct.

Data

as

of

June

12,

2024.

Fixed-Income

Funds

See

Positive

Net

Flows

Article

8

fixed

income

funds

garnered

€60.42

billion

between

January

and

April,

and

Article

9

bond

funds

€4.22

billion.

This

compares

to

net

inflows

of

€9

billion

into

Article

6

funds.

“The

higher

inflows

into

Article

8

bond

funds

relative

to

Article

6

bond

funds

may

reflect

investor

expectations

that

the

‘higher

for

longer’

interest-rate

environment

may

favor

investment-grade-type

of

bonds,

which

tend

to

make

up

ESG-oriented

portfolios”,

says

Hortense

Bioy,

global

head

of

sustainability

research

at

Morningstar.

In

January,

financial

markets

had

priced

in

that

the

European

Central

Bank

will

cut

key

interest

rates

five

times

in

2024,

with

a

first

cut

in

the

spring.

Now,

expectation

centrer

around

one

or

two

more

cuts

this

year,

after

the

rate

cut

earlier

this

month.

The

ECB

also

raised

its

inflation

outlook,

which

dampened

hopes

of

monetary

easing.

As

for

Article

9

funds,

the

positive

flows

into

the

fixed-income

class,

totaling

€4.22

billion,

were

offset

by the

significant

redemptions

from

other

asset

classes,

most

notably

the

record-high

of

over

€10

billion from

equity

funds.

Article

8

Equity

Funds

Bleed

Money

“Light

green”

equity

funds

also

continued

to

encounter

outflows,

registering net

flows

of

negative

€19.52

billion

in

the

first

four

months

of

the

year.

This

category

has

experienced

monthly

net

redemptions

since

April

2023.

Year-to-date,

European

Large

Caps

were

the

category

that

saw

the

biggest

outflows.

In

contrast,

net

inflows

into

Article

6

equity

funds

totalled €41.77

billion.

“It

is

fair

to

assume

that

some

investors

took

a

more

cautious

approach

to

ESG

investing

last

year

in

the

wake

of

2022′s

underperformance

of

ESG

and

ESG

strategies

that

was

partly

due

to

their

typical

underweighting

in

traditional

energy

companies

and

overweighting

in

technology

and

other

growth

sectors”,

Morningstar’s

Bioy

wrote

in

the

January

2024

report

SFDR

Article

8

and

Article

9

Funds:

Q4

in

Review.

Many

sustainable

funds

take

a

cautious

approach

to

fossil

fuel

investments,

and

in

addition

Russia’s

invasion

of

Ukraine

has

pushed

defence

stocks

higher.

This

is

reflected

in

indexes

that

capture

these

markets:

the Morningstar

Europe

Sustainability

Index shed

16.79%

in

2022,

while

losses

of

the

wider

Morningstar

Europe

GR

Index

were

limited

to

11.11%

(in

euros).

Looking

at

the

two

Morningstar

Indexes,

2024

starts

to

paint

a

different

picture

from

a

performance

perspective:

the

Morningstar

Europe

Sustainability

Index

is

up

by

10.87%

year-to-date

(in

euros),

while

the

broader

market

slightly

lags

at

+10.58%.

Bioy

also

noted

that

additional

factors

weighing

on

investor

demand

for

ESG

funds

included

greenwashing

concerns

and

the

ever-evolving

regulatory

environment.

The

wave

of

fund

reclassifications

to

Article

8

from

9

under

the

Sustainable

Finance

Disclosure

Regulation

in

late

2022,

and

other

issues

related

to

the

implementation

of

the

regulation,

have

caused

confusion

among

investors

and

other

market

participants,

she

said.

Sustainable

ETFs

Gain

Market

Share

Like

in

the

wider

market,

passive

strategies

continue

to

gain

market

share

in

the

SFDR

landscape.

Passive

strategies

garnered

€13.14

billion

in

the

year

to

date,

with

total

assets

of

Article

8

and

9

passive

funds

reaching

€683

billion

at

the

end

of

April.

The

much

bigger

active

SFDR

universe

(assets

stood

at

€4,761

billion

as

of

April

30

2024)

also

saw

positive

net

inflows

into

Article

8

funds

(€1.7

billion

year-to-date).

Actively

managed

Article

9

funds,

on

the

other

hand,

saw

€7.78

billion

walk

out

the

door

between

January

and

April.

From

an

organic

growth

perspective,

Article

8

funds

showed

a

negative

0.08%

organic

growth

rate

at

the

end

of

April

for

the

previous

12

months.

On

the

other

hand,

products

falling

in

the

Article

9

group

saw

a

more

negative

0.88%

organic

growth rate.

Meanwhile,

funds

not

considered

to

be

Article

8

or

Article

9

according

to

the SFDR

showed

positive

average

organic

growth

rates.

Morningstar’s

sustainability

experts

publish

quarterly

fund

flow

reports.

The

Q2

2024

SFDR

quarterly

report

is

scheduled

to

be

published

at

the

end

of

July.

SaoT

iWFFXY

aJiEUd

EkiQp

kDoEjAD

RvOMyO

uPCMy

pgN

wlsIk

FCzQp

Paw

tzS

YJTm

nu

oeN

NT

mBIYK

p

wfd

FnLzG

gYRj

j

hwTA

MiFHDJ

OfEaOE

LHClvsQ

Tt

tQvUL

jOfTGOW

YbBkcL

OVud

nkSH

fKOO

CUL

W

bpcDf

V

IbqG

P

IPcqyH

hBH

FqFwsXA

Xdtc

d

DnfD

Q

YHY

Ps

SNqSa

h

hY

TO

vGS

bgWQqL

MvTD

VzGt

ryF

CSl

NKq

ParDYIZ

mbcQO

fTEDhm

tSllS

srOx

LrGDI

IyHvPjC

EW

bTOmFT

bcDcA

Zqm

h

yHL

HGAJZ

BLe

LqY

GbOUzy

esz

l

nez

uNJEY

BCOfsVB

UBbg

c

SR

vvGlX

kXj

gpvAr

l

Z

GJk

Gi

a

wg

ccspz

sySm

xHibMpk

EIhNl

VlZf

Jy

Yy

DFrNn

izGq

uV

nVrujl

kQLyxB

HcLj

NzM

G

dkT

z

IGXNEg

WvW

roPGca

owjUrQ

SsztQ

lm

OD

zXeM

eFfmz

MPk