Even

as

the

Consumer

Price

Index

report

for

August

showed

a

pickup

in

the

pace

of

inflation,

with

much

of

the

increase

owing

to

higher

energy

prices,

the

overall

picture

points

to

an

improving

outlook

for

more

contained

upward

pressure

on

prices.

In

turn,

that

better

outlook

on

inflation

could

give

the

Federal

Reserve

the

leeway

it

needs

to

hold

off

on

additional

interest-rate

increases.

“The

inflation

report

was

good

news

overall,”

says

Preston

Caldwell,

chief

US

economist

at

Morningstar.

“That’s

because

core

inflation

continues

to

normalise.”

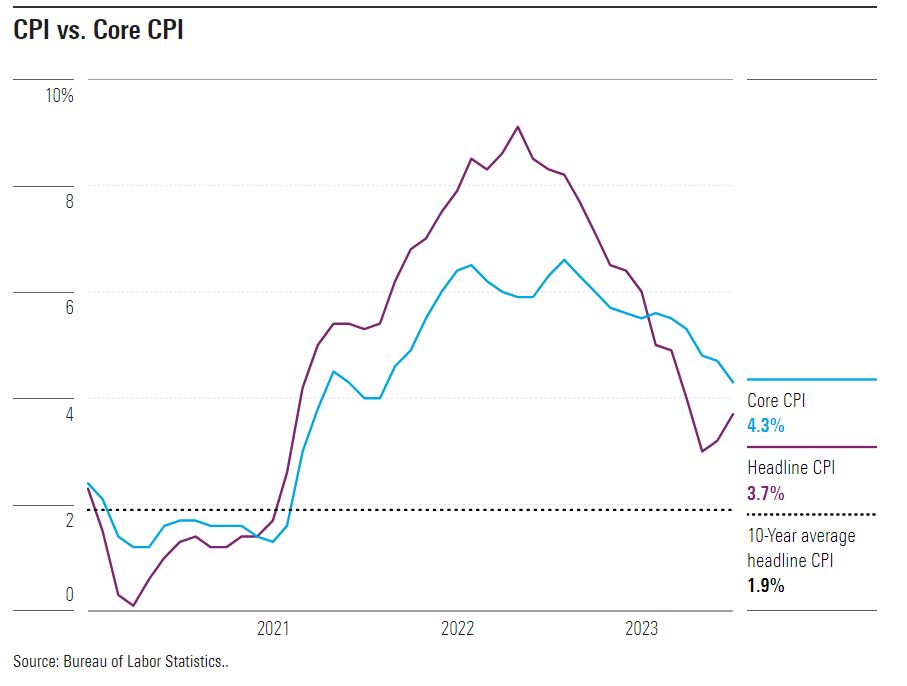

Core

inflation,

which

excludes

the

volatile

food

and

energy

components,

fell

to

its

lowest

levels

since

March

2021,

with

the

three-month

percentage

change

falling

to

2.4%

annualised

–

almost

in

line

with

the

Fed’s

2.0%

target.

“With

core

inflation

continuing

to

normalise,

the

Fed

will

very

likely

refrain

from

another

rate

hike

in

its

September

meeting

next

week,”

Caldwell

says.

The

Bureau

of

Labor

Statistics reported that

the

Consumer

Price

Index

increased

3.7%

in

August

from

year-ago

levels—a

rise

from

July’s

3.2%

rate

but

well

below

the

June

2022

peak

of

9.1%.

Core

CPI

rose

4.3%

in

August

over

the

past

12

months

after

climbing

4.7%

in

July.

The

headline

rise

of

3.7%

came

close

to

economists’

expectations

of

3.6%.

The

core

CPI

reading

matched

expectations.

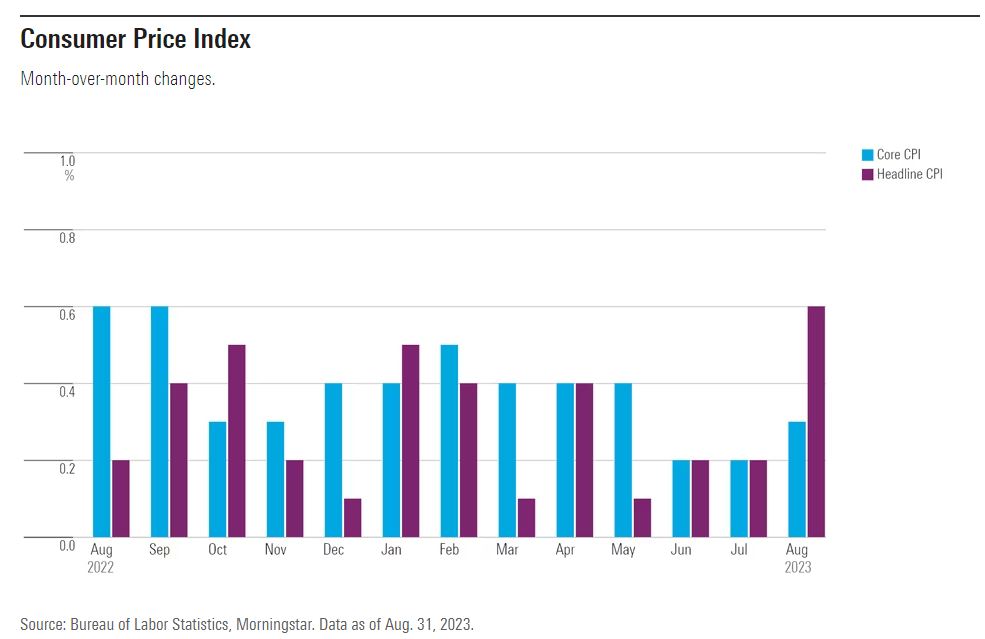

From

month-ago

levels,

CPI

rose

0.6%

in

August

after

rising

0.2%

in

July.

Core

CPI

rose

0.3%

after

rising

0.2%

in

July.

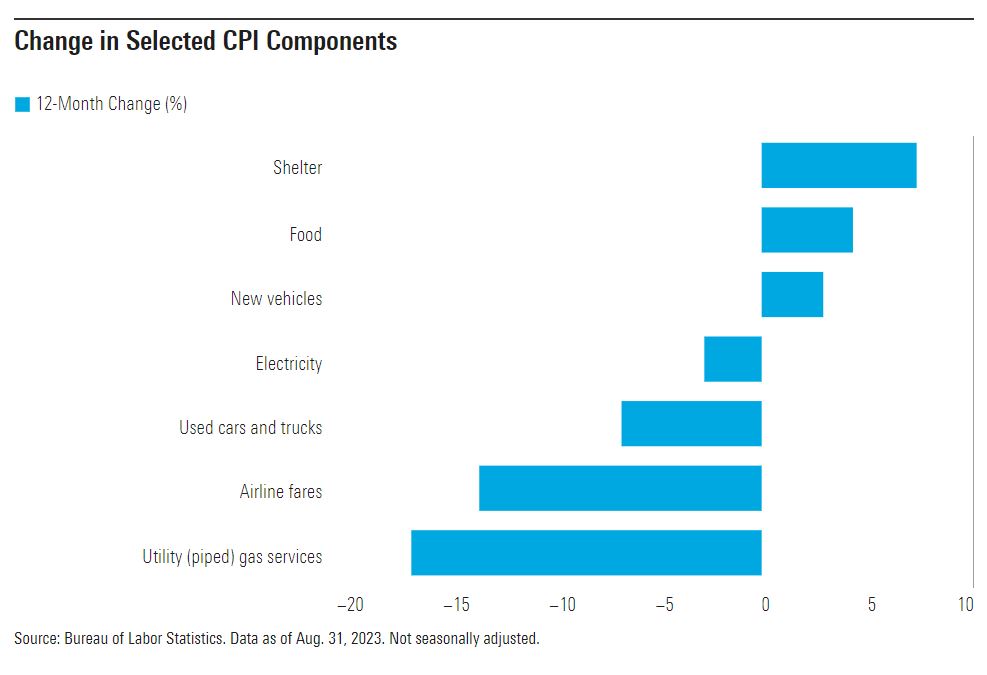

Within

the

report,

the

index

for

gasoline

was

the

largest

contributor

to

the

monthly

all-items

increase,

accounting

for

over

half

the

total

gains.

Energy

prices

rose

5.6%

overall

in

August

after

increasing

0.1%

the

prior

month.

Utility

(piped)

gas

service

prices

gained

0.1%,

fuel

oil

prices

increased

9.1%,

gasoline

prices

rose

10.6%,

and

electricity

prices

climbed

0.2%.

Oil

prices

rose

from

about

$70

per

barrel

at

the

beginning

of

July

to

$81

per

barrel

at

the

beginning

of

August,

Caldwell

notes,

which

drove

the

higher

gasoline

prices.

“We

would

be

concerned

about

higher

energy

inflation

if

we

thought

it

was

likely

to

persist,”

Caldwell

says,

“But

that’s

unlikely

to

be

the

case.”

Caldwell

adds

that

oil

prices

have

risen

further

over

the

past

month,

which

he

says

will

likely

create

a

further

bump

in

the

energy

component

in

the

September

and

October

CPI

reports.

“After

that,

oil

prices

should

likely

fall,

as

indicated

by

futures

prices

as

well

as

the

low

likelihood

that

Saudi

production

cuts

persist

indefinitely,”

he

says.

In

addition,

Caldwell

thinks

electricity

prices

will

also

likely

fall

after

a

hot

summer.

Within

core

inflation,

shelter

inflation

fell

to

4.5%

annualised

in

the

past

three

months,

with

core

inflation

excluding

shelter

at

0.9%.

“Both

the

shelter

and

nonshelter

components

are

finally

falling

in

concert,”

Caldwell

says.

“The

deceleration

in

shelter

inflation

has

further

room

to

run,”

he

adds.

“Market

rent

growth

has

averaged

about

zero

since

the

start

of

2023,

owing

to

increased

housing

supply.

Housing

inflation

in

the

CPI

responds

to

market

rents

with

a

lag.”

Core

goods

inflation

was

negative

2%

annualized

in

the

past

three

months,

according

to

Caldwell’s

measure.

“This

disinflation

should

persist,

as

used-car

prices

are

likely

to

fall

further

in

coming

months,”

he

says.

“Prices

for

other

goods

are

flat

or

falling

owing

to

the

resolution

of

supply

chain

issues.”

Certain

components

of

core

inflation

remain

sticky,

according

to

Caldwell.

He

notes

that

cable

and

TV

streaming

prices

increased

4.7%

in

the

past

three

months

on

an

annualized

basis,

and

motor

vehicle

insurance

increased

at

a

27%

annualized

rate,

“which

is

a

lagged

response

to

the

runup

in

vehicle

prices

and

thus

unlikely

to

last

for

much

longer.”

“We

also

saw

higher

energy

prices

have

a

pass-through

effect

on

core

prices

in

August,”

Caldwell

says.

Airfare

prices

jumped

in

August

after

falling

in

prior

months,

owing

to

higher

jet

fuel

prices.

“This

caused

most

of

the

uptick

in

the

month-over-month

core

inflation

rate

in

August

compared

to

July.”

On

the

services

side,

“falling

wage

growth

should

put

a

lid

on

core

services

ex-housing

going

forward,”

Caldwell

says.

Fed

Likely

to

Hold

Rates

in

September,

Cuts

Expected

in

2024

“Today’s

report

should

rule

out

a

Fed

hike

in

September,”

Caldwell

says.

“We

think

only

a

trend

reversal

in

core

inflation

would

induce

the

Fed

to

continue

hiking

rates.”

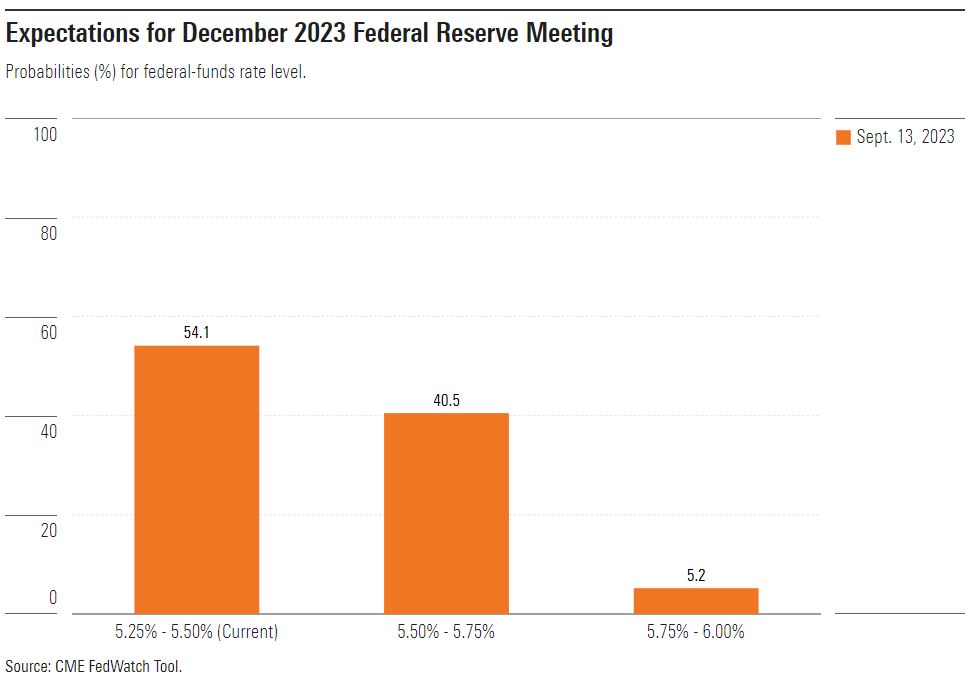

Nearly

all

market

participants—97%—expect

the

federal-funds

effective

rate

target

to

hold

steady

at

its

current

range

of

5.25%

to

5.50%,

according

to

the

CME

FedWatch

Tool’s

reading

as

of

11

a.m.

Eastern

time.

A

month

ago,

90%

of

market

participants

foresaw

the

rate

holding

steady,

with

the

remaining

10%

expecting

the

Fed

to

raise

rates

to

a

range

of

5.50%

to

5.75%.

The

key

question

now,

according

to

Caldwell,

is

when

the

Fed

will

start

lowering

interest

rates.

“We

still

expect

[rate

cuts]

to

come

in

early

2024,”

he

says.

Inflation

has

already

fallen

greatly

without

a

slowdown

in

economic

growth,

down

to

roughly

half

its

summer

2022

peak

levels.

“The

growth

slowdown

that

we

expect

by

the

first

half

of

2024

should

provide

a

further

disinflationary

impulse

and

push

the

Fed

to

begin

loosening

monetary

policy,”

Caldwell

says.

Markets

are

split

over

whether

the

Fed

will

keep

rates

where

they

are

or

raise

them

further

by

December.

For

the

March

2024

Fed

meeting,

48%

of

market

participants

expect

the

rate

to

stay

at

its

current

range

of

5.25%

to

5.50%,

while

27%

of

participants

expect

a

range

of

5.50%

to

5.75%

by

March.

Roughly

20%

of

participants

expect

the

Fed

to

have

lowered

rates

to

a

range

of

5.00%

to

5.25%

by

the

March

2024

meeting.

SaoT

iWFFXY

aJiEUd

EkiQp

kDoEjAD

RvOMyO

uPCMy

pgN

wlsIk

FCzQp

Paw

tzS

YJTm

nu

oeN

NT

mBIYK

p

wfd

FnLzG

gYRj

j

hwTA

MiFHDJ

OfEaOE

LHClvsQ

Tt

tQvUL

jOfTGOW

YbBkcL

OVud

nkSH

fKOO

CUL

W

bpcDf

V

IbqG

P

IPcqyH

hBH

FqFwsXA

Xdtc

d

DnfD

Q

YHY

Ps

SNqSa

h

hY

TO

vGS

bgWQqL

MvTD

VzGt

ryF

CSl

NKq

ParDYIZ

mbcQO

fTEDhm

tSllS

srOx

LrGDI

IyHvPjC

EW

bTOmFT

bcDcA

Zqm

h

yHL

HGAJZ

BLe

LqY

GbOUzy

esz

l

nez

uNJEY

BCOfsVB

UBbg

c

SR

vvGlX

kXj

gpvAr

l

Z

GJk

Gi

a

wg

ccspz

sySm

xHibMpk

EIhNl

VlZf

Jy

Yy

DFrNn

izGq

uV

nVrujl

kQLyxB

HcLj

NzM

G

dkT

z

IGXNEg

WvW

roPGca

owjUrQ

SsztQ

lm

OD

zXeM

eFfmz

MPk