Step

into

a

time

machine

and

travel

back

30

years

to

March

1,

1994.

Emerging

markets

equity

funds

have

become

the

exciting

new

investment,

and

mutual

funds

the

way

to

own

them.

For

a

small

annual

fee,

investors

can

participate

in

the

rapid

growth

of

such

countries,

while

diversifying

their

risks

among

dozens

of

holdings

and

benefiting

from

professional

management.

What

an

opportunity!

One

thing

was

for

certain:

better

stocks

than

bonds.

Sure,

emerging

markets

bonds

figured

to

outgain

their

domestic

counterparts

because

greater

risk

eventually

creates

greater

rewards,

but

when

investing

in

high-growth

areas,

why

buy

debt?

After

all,

nobody

ever

got

rich

buying

bonds

from

Walmart

(WMT)

or

Microsoft

(MSFT).

The

path

to

riches

comes

from

ownership,

not

lending.

What

Happened

to

Emerging

Markets

in

Reality

Or

so

the

theory

went.

The

practice

was

very,

very

different.

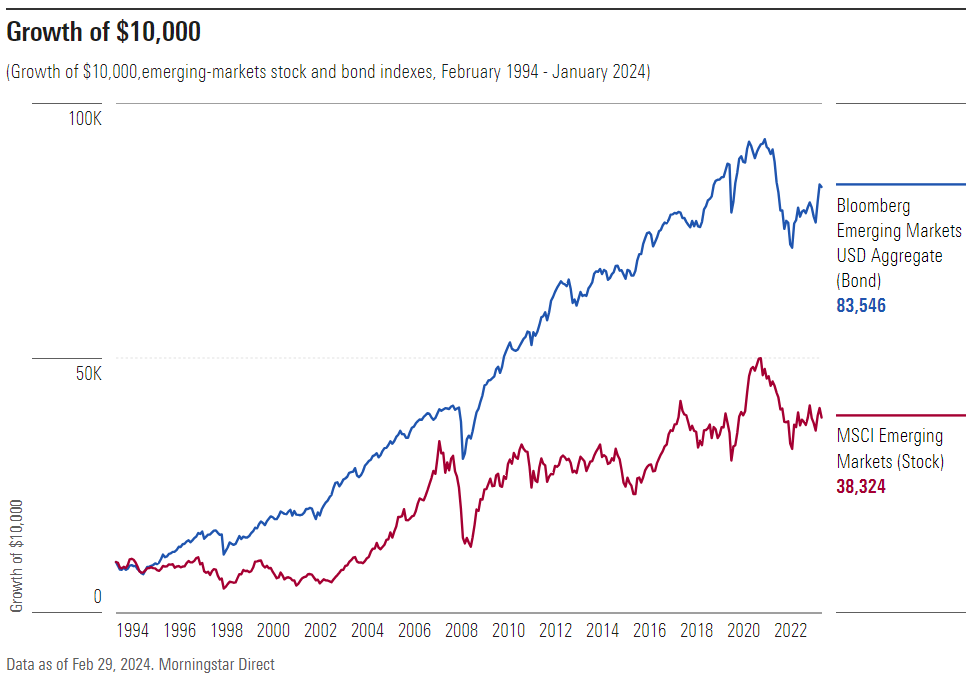

Below

are

the

30-year

returns,

since

February

1994,

for

1)

MSCI

Emerging

Markets

Index,

which

contains

stocks,

and

2)

Bloomberg

Emerging

Markets

USD

Aggregate

Index,

which

holds

bonds.

The

Bloomberg

index

appears

in

blue

and

MSCI

in

red.

Well

now.

As

you

may

have

heard

in

modern

US

history,

bonds

have

never

outgained

equities

over

any

30-year

period.

(That

statement

does

not

apply

for

the

nation’s

earlier

history,

though.)

But

they

certainly

have

done

so

with

emerging

markets.

Bonds

started

off

ahead,

conceded

some

of

their

lead

in

the

mid-2000s,

recovered

their

lost

ground

in

2008,

and

have

not

since

looked

back.

During

the

30-year

period,

the

annualised

total

return

for

Bloomberg’s

bond

index

was

7.33%,

as

opposed

to

4.58%

for

MSCI’s

stock

index.

So

much

for

the

equity

risk

premium!

The

contest

was

not

even

close.

Through

the

30

years,

bonds

triumphed

by

a

whopping

2.75

percentage

points

per

year.

Dollar

Bashing

and

Emerging

Market

Tension

One

potential

explanation

for

this

anomaly

is

the

strength

of

the

US

dollar.

Although

the

business

press

has

long

bemoaned

America’s

“weak

dollar”

policy –

a

habit

that

reached

its

apex

when

The

Wall

Street

Journal

praised

Heidi

Klum

for

choosing

to

be

paid

in

euros

rather

than

dollars –

their

forecasts

have,

in

fact,

been

grievously

wrong.

Last

year,

the

US

Dollar

Index

reached

a

20-year

high.

That

matters

because

emerging

markets

bonds

have

historically

been

denominated

primarily

in

dollars.

Through

the

early

2000s,

almost

all

foreign-held

debt

from

emerging

nations

consisted

of

US

dollar

bonds.

That

percentage

has

since

declined

to

about

60%,

but

nonetheless,

emerging

markets

debt

has

largely

been

protected

against

the

dollar’s

rise.

Not

so

for

its

equity

rivals.

That

condition,

however,

only

accounts

for

about

one

percentage

point

of

the

annualised

performance

gap,

which

still

leaves

emerging

markets

stocks

well

behind

their

fixed

income

rivals.

To

that

handicap

may

be

added

the

International

Monetary

Fund’s

assessment

that

a

strong

dollar

slows

the

relative

growth

of

emerging

markets

economies

by

reducing

their

trade

volumes

and

squeezing

credit.

That

may

have

cost

emerging-markets

stocks

a

further

percentage

point.

Has

There

Been

an

Emerging

Market

Boom?

Of

course,

the

dollar’s

strength

notwithstanding,

most

of

the

emerging

markets

have

handsomely

expanded

their

economies.

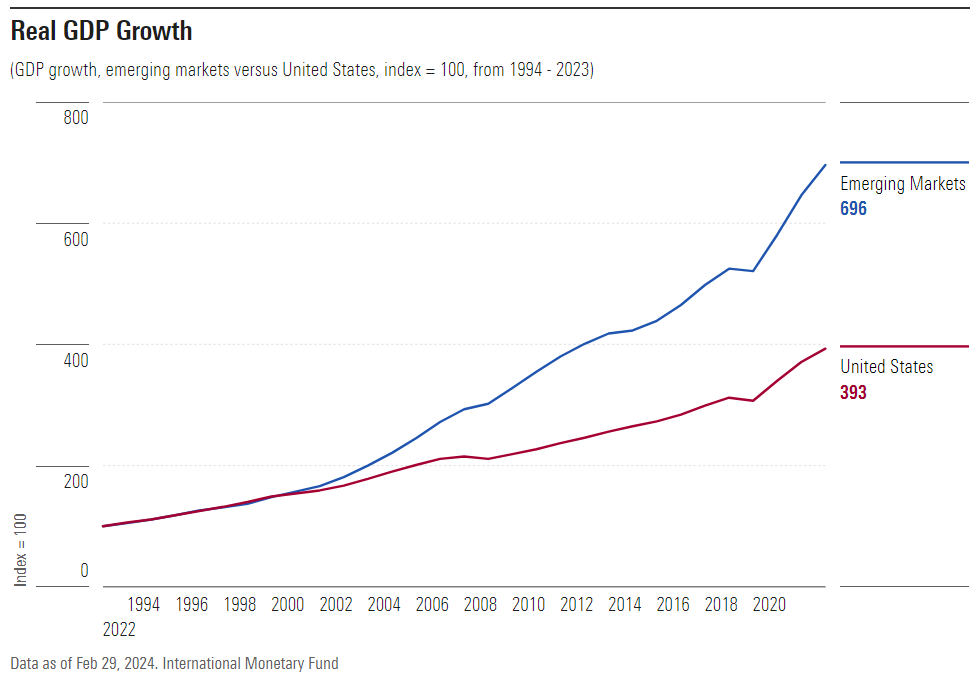

According

to

the

IMF’s

data,

real

gross

domestic

product

growth

for

the

emerging

markets

has

substantially

exceeded

that

of

the

United

States

since

1993,

even

when

converting

those

figures

into

dollars.

Admittedly,

this

comparison

is

incomplete

because

it

ignores

population

changes.

As

the

emerging

markets

have

increased

their

populations

more

rapidly

than

has

the

US,

they

could

conceivably

have

posted

faster

GDP

growth

while

not

improving

individual

productivity.

That,

however,

has

not

been

the

case.

When

scored

by

GDP

per

capita,

the

emerging

markets

have

been

superior.

No

matter

what

the

measurement,

they

have

delivered

on

the

promise

that

equity

investors

so

dearly

prized

30

years

ago:

speedier

economic

growth.

Considering

Valuations

A

final

potential

explanation

for

the

struggles

of

emerging

markets

stocks

is

lower

valuations.

If

emerging

markets

equities

were

costly

in

1994

and

have

since

become

cheap,

that

markdown

could

have

sharply

affected

their

returns.

That

process

did

occur,

but

only

mildly.

In

1994,

reports

the

investment

management

firm

Schroders

(SDR),

the

price/earnings

ratio

for

emerging

markets

stocks,

based

on

the

next

12

months’

forecasted

results,

was

16.

Today,

that

figure

is

12.

That

effect,

once

again,

amounts

to

about

onew

percentage

point

a

year.

Emerging

Markets:

The

Postmortem

Over

the

past

30

years,

emerging

markets

stocks

have

shed

an

annual

percentage

point

of

performance

to

each

of

three

items:

1)

direct

currency

losses;

2)

indirect

currency

headwinds;

and

3)

reduced

investment

valuations.

In

aggregate,

those

factors

account

for

the

discrepancy

between

emerging-markets

stocks

and

bonds.

Had

they

not

occurred,

returns

for

the

two

asset

classes

would

have

been

similar.

Which

leaves

us

with

a

mystery.

Stocks

are

supposed

to

outgain

bonds

over

three

decades,

particularly

when

their

economies,

as

represented

by

GDP

growth

rates,

have

been

outstanding.

So,

as

well,

has

been

the

political

news.

By

and

large,

the

major

emerging

markets

have

been

war-free,

with

stable

governments.

The

conditions

have

been

seemingly

ideal –

yet

even

when

appraised

generously,

the

equities

from

those

countries

have

not

been

able

to

beat

bonds.

What

happened?

That

question

I

cannot

fully

answer.

I

will

offer

two

partial

responses,

though.

First,

emergingmarkets

companies

are

better

at

booking

revenues

than

profits.

A

few

years

ago,

McKinsey

estimated

returns

on

invested

capital

were

50%

higher

for

North

American

businesses

than

for

their

emerging

markets

competitors.

Second,

honesty

pays

with

investing.

In

general,

countries

that

score

well

on

Transparency

International’s

Corruption

Perceptions

Index

have

enjoyed

higher

stock

market

returns.

Few

of

those

nations

are

emerging.

Emerging

Markets:

Promises

Not

Kept?

History

may

not

repeat.

The

dollar

could

weaken,

the

price/earnings

ratios

for

emerging

markets

stocks

could

rise,

and

profit

margins

could

strengthen.

For

those

reasons

and

more,

many

investment

forecasters

now

expect

emerging

markets

stocks

to

outgain

their

developed

market

rivals.

Perhaps.

Unfortunately,

such

claims

are

not

new.

For

many

years

now,

emerging

markets

optimists

have

issued

such

prophecies.

They

have

yet

to

transpire.

Eventually,

emerging

markets

equities

will

recover

from

their

funk.

Whether

that

makes

the

asset

class

worth

owning

is,

however,

another

story.

I

remain

skeptical.

The

author

or

authors

do

not

own

shares

in

any

securities

mentioned

in

this

article. This

article

was

originally

published

on

Morningstar.com

for

a

US

audience.

SaoT

iWFFXY

aJiEUd

EkiQp

kDoEjAD

RvOMyO

uPCMy

pgN

wlsIk

FCzQp

Paw

tzS

YJTm

nu

oeN

NT

mBIYK

p

wfd

FnLzG

gYRj

j

hwTA

MiFHDJ

OfEaOE

LHClvsQ

Tt

tQvUL

jOfTGOW

YbBkcL

OVud

nkSH

fKOO

CUL

W

bpcDf

V

IbqG

P

IPcqyH

hBH

FqFwsXA

Xdtc

d

DnfD

Q

YHY

Ps

SNqSa

h

hY

TO

vGS

bgWQqL

MvTD

VzGt

ryF

CSl

NKq

ParDYIZ

mbcQO

fTEDhm

tSllS

srOx

LrGDI

IyHvPjC

EW

bTOmFT

bcDcA

Zqm

h

yHL

HGAJZ

BLe

LqY

GbOUzy

esz

l

nez

uNJEY

BCOfsVB

UBbg

c

SR

vvGlX

kXj

gpvAr

l

Z

GJk

Gi

a

wg

ccspz

sySm

xHibMpk

EIhNl

VlZf

Jy

Yy

DFrNn

izGq

uV

nVrujl

kQLyxB

HcLj

NzM

G

dkT

z

IGXNEg

WvW

roPGca

owjUrQ

SsztQ

lm

OD

zXeM

eFfmz

MPk